Should congress give the Big Three automakers $25 billion to try to stave off bankruptcy? How should I know! There are too many unknowns for me to be able to construct an informed opinion. By the time I do enough research to begin to figure out what's really going on, we will have moved on to the next issue. I just hope the people making the decisions in Washington know what they're doing.

I've watched excerpts from a couple of congressional hearings where our representatives criticize the automaker CEOs for coming to Washington in separate private jets. (Is this like not wearing a flag lapel pin? Is this really about political correctness?) Everyone seems pretty down on these executives, as if they're personally responsible for driving their companies into the ground. Are they? Have they? Or, are we just mad that they make so much money?

Maybe they just make the cars people want to buy. It's certainly true that they can't build a 'green' car that people don't want and sell it at a price people aren't willing to pay. Or maybe they spend the big advertising bucks to convince us that we want to buy the cars they want to make. Is it that they aren't building the cars that people want to buy? Or, is nobody buying cars?

For the sake of argument, let's say nobody's buying cars. If that's the case, what do we expect from our automakers? Do we expect them to hibernate until we get past this recession, or at least past the credit crunch? Should they be crushed by the Invisible Hand of the Free Market or are they

too big to fail?

Chapter 11 is supposed to handle situations where a business has just gotten in over its head and, if reorganized, can get back on its feet. But, if none of the car companies are selling cars how would reorganization help? Some say people won't buy a car from a bankrupt company and that, Chapter 11 would lead to

Chapter 7, and that would be the end of the company, causing a domino effect through all the other companies that are linked by doing business together - millions of people out of work! Are these companies

too big to fail?

What does that mean for a company to be too big to fail? Does it mean the United States government must guarantee its survival? If that's the case, this has got to work in some way other than these companies just coming to us for money whenever things don't go their way. I'm not sure these CEOs have even brought a plan with them to show how this $25 billion is going to help.

If a company is too big to fail and the taxpayers are going to be responsible for rescuing it when it gets into trouble, then I expect my government to do everything it can to make sure it doesn't get in trouble. This means regulations and oversight, maybe not allowing a company to get to the point where its that important.

For a guy who started out saying he didn't know enough to have an informed opinion, here I am talking about government regulation of big business like I was some kind of expert! You know how pretty soon after the polls close on election night, the networks announce that, "with one percent of the votes counted, we're calling the election for Joe Blow", or whomever? When I start thinking I can solve the automakers' problems, there ought to be a little announcer in my head saying "with one percent of the facts in, we're declaring the solution to be..."

I can't help but have lots of uninformed opinions. People who reinforce what I already think look smart; those who disagree make me uncomfortable. But I think I'm going to have to rely on my representatives in Washington to figure out what to do.

One more thing. Conservatives, opposed to government action in response to this crisis, who justify their objections using axioms or aphorisms, are not persuasive. These platitudes oversimplify the situation in order to make it easier to understand and to justify the use of stock responses. It's important that we deal with the the entire complexity of problems that confront us, not symbolic caricatures that only capacitate the ideology of one segment of society.

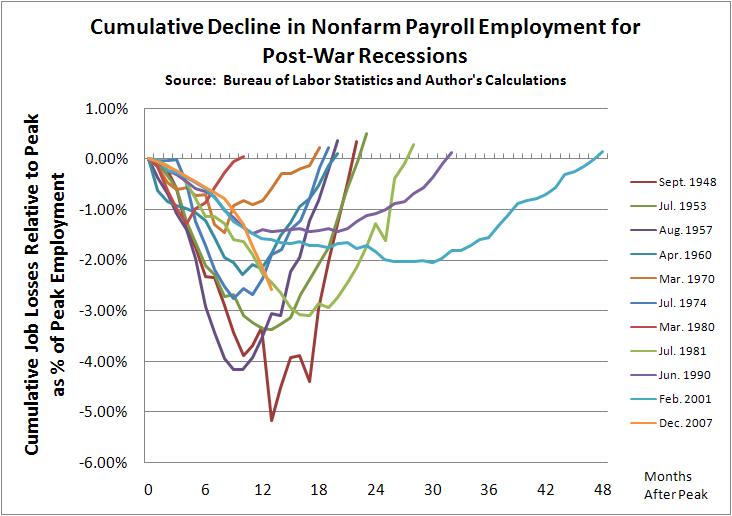

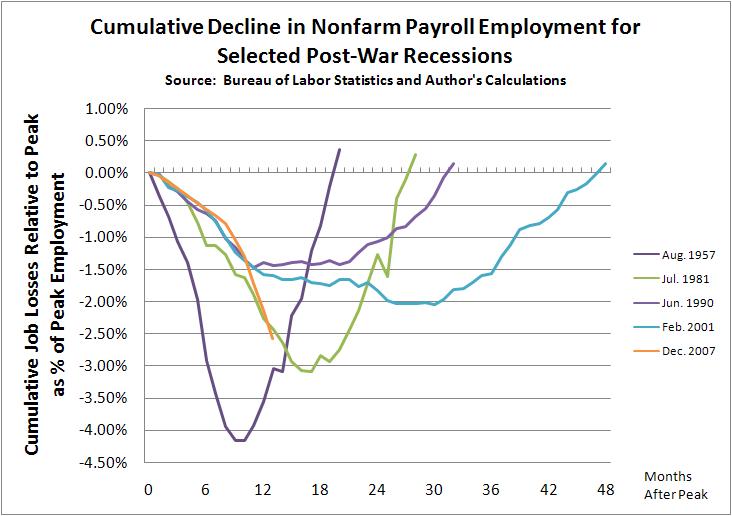

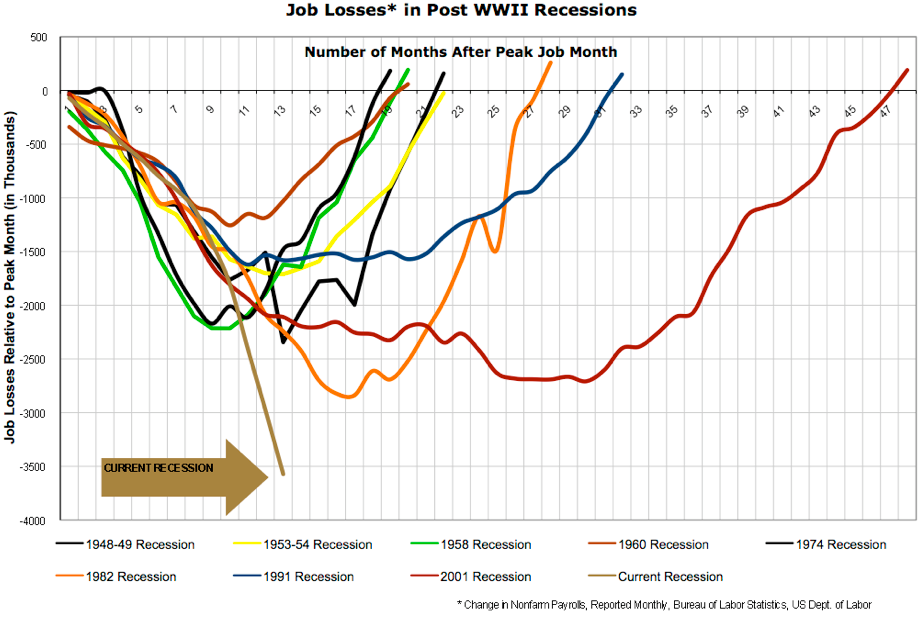

The next chart is slightly different, showing the number of jobs lost, rather than the percentage. Since the population and economy have both been growing since WWII, the current recession effects more jobs and people than earlier, but similarly deep, recessions.

The next chart is slightly different, showing the number of jobs lost, rather than the percentage. Since the population and economy have both been growing since WWII, the current recession effects more jobs and people than earlier, but similarly deep, recessions.

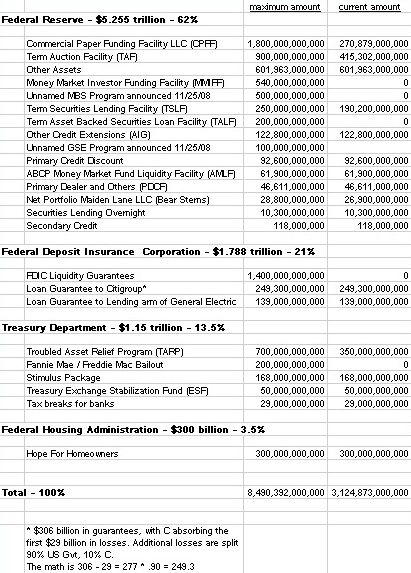

The above is already out of date. The $4.6 trillion was as of November. (From

The above is already out of date. The $4.6 trillion was as of November. (From